For most, this question is easy to answer: A 1035 Exchange can avoid any taxable events, and the funds are transferred directly from one insurance company to another, making it a superior choice for most. However, while that is technically accurate, it says nothing about it being the best way to transfer cash value from one policy to another. That’s a different question entirely.

The answer to the question of the best way to transfer cash value from one policy to another and myriad other questions in any planning discussion is simple: It depends.

The best answers depend on the specifics of the client’s circumstances, the assets involved, the desired outcome, and an evaluation of the various alternatives available in the market. They can also be completely counter to the conventional wisdom around the topic, and 1035 exchanges are a great example.

On the surface, they’re simple. However, their superiority is frequently tied to tax avoidance. While that is certainly a worthy objective, it does assume there are taxes due in the first place. If there’s no gain in the contract, is an exchange really necessary? Why not surrender the policy and then use the proceeds to fund the new insurance? At first blush, this may seem to be a distinction without a difference except perhaps convenience.

Does it really matter how the cash value transfers? It can, and for reasons that may not be readily apparent.

Here’s an Example

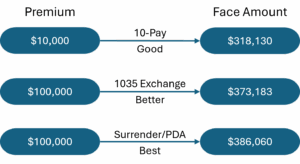

Consider a 55-year-old male, Preferred Non-Smoker with $100,000 in surrender value and no gain. A quick survey of the market points to a new policy with a face amount of $373,183 funded via 1035 Exchange. A solid solution, but not the best.

That insurance company also offers a Premium Deposit Account, or PDA. What’s a PDA? It’s an account at an insurance company offered as a place to “park” some cash, generate interest and fund future premiums. The fact that it pays interest is what makes this interesting.

Figure 1: Case Design Alternatives

How interesting? How about an additional $12,877 in coverage, an increase of 3.4%? That’s the best solution.

Of course, this is a bit like we’re leaning over the balcony to see the ocean view from a hotel room. That said, a difference of 3.4% can be the difference between being able to improve a client’s position and recommending they retain their policy.

This is just one use of a PDA. It happens to be the one that doesn’t require the client to come out of pocket for a single pay premium. If the client has the cash flow to fund a single premium, PDA accounts can also be used to acquire larger coverage amounts or increase the efficiency of protection and accumulation designs. As an example, in the case mentioned above, a $10,000 ten-pay protection-focused design without the PDA only results in $318,130 in coverage, the worst outcome of the three options! In an accumulation design, the use of the PDA results in a nearly 22% increase in income. Also important: PDAs can’t be used with a 1035 Exchange. Those transactions require all funds be deposited into the policy immediately upon receipt.

Finally, there is an exciting near-term opportunity involving an insurance company with a 12% first year rate on their PDA. That may be enough to go from interesting to exciting. How interesting? Existing insurance policies with as much as 25% in taxable gain could still benefit from a surrender and PDA funding versus a 1035!

Have questions or want to discuss how this applies to your clients? Reach out to your Cavalier Associates Marketing Consultant for additional information.

Not sure who to contact? Please call the office @ (800) 350-2019 for assistance.

Related Articles

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.