A Practical Way to Manage Market Entry Timing in FIAs

A 90-day low-point window can help manage market entry risk in single-premium FIAs without adding cost or complexity.

Advisors know market timing is rarely perfect, especially when a client is committing a meaningful lump sum. Even when the long-term strategy makes sense, a market dip shortly after issue can create frustration and second-guessing that’s hard to unwind.

This dynamic shows up frequently in fixed indexed annuities, where the starting point of the first index segment can shape how a client feels about the decision early on. Managing that initial experience matters, not just for performance, but for confidence.

Some FIA designs address this directly with a 90-day low-point window.

How the 90-Day Low-Point Window Works

The index segment starts the same way it does in a traditional FIA. What’s different is what happens next.

After the segment begins, the contract opens a 90-day observation window. During that period:

– The index is monitored daily

– If the index hits a lower value, that lower value becomes the starting point

– If it doesn’t, the original start date stays in place

There’s nothing for the client to decide and nothing for the advisor to manage. The adjustment, if it occurs, happens automatically. If it doesn’t, the contract behaves exactly like a standard FIA.

Why This Matters in Practice

Early market declines are one of the most common sources of client frustration after a lump-sum allocation. Even when results even out over time, that early experience can linger.

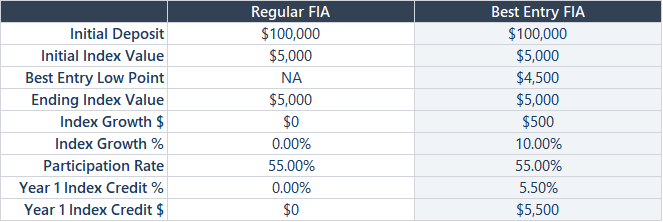

Assume a $100,000 single-premium FIA where the index drops 10% during the first 90 days and then finishes the year flat relative to the original start date.

Without a low-point feature, that’s a zero-credit year.

With the low-point adjustment, the recovery is measured from a lower starting value, turning that same flat year into a positive index credit.

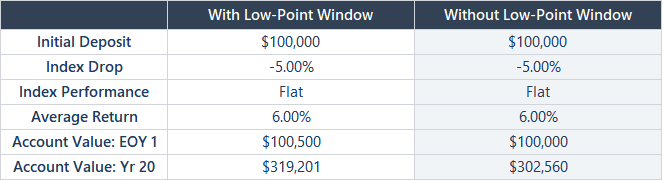

Table 1: Increased First-Year Index Credit

In this scenario, a year that would have produced no gain instead results in a 5.5% credit.

The Longer-Term Impact

That early difference may not feel dramatic, but it compounds.

Assuming a 6.0% long-term rate of return, starting from a lower entry point can translate into more than $16,000 of additional account value by year 20.

Table 2: Increased Account Values

This isn’t about chasing returns. It’s about improving the starting conditions and letting time do the rest.

What If the Market Never Drops?

If the index never trades below the initial value during the 90-day window, the feature simply doesn’t come into play. The FIA performs just like any other.

There’s:

– No downside

– No opportunity cost

– No additional fee or rider charge

In other words, it only matters when it helps.

Putting It to Work in Client Conversations

This approach isn’t meant to predict markets or add complexity. It’s a practical way to reduce the impact of poor timing, something neither advisors nor clients can control.

In designs that also include competitive index crediting options and a strong, fee-free bonus, this structure can further improve early contract value while keeping the overall strategy clean.

For advisors working with single-premium allocations, a 90-day low-point window offers a straightforward way to address a common client concern and set expectations more effectively from day one.

Have questions or want to discuss how this applies to your clients? Reach out to your Cavalier Associates Marketing Consultant for additional information.

Not sure who to contact? Please call the office @ (800) 350-2019 for assistance.

Related Articles

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.