One of the fundamental elements of financial planning is matching client risk tolerance and time horizons to a suitable product solution. That can become challenging when the client’s true appetite for risk lies somewhere between the available solutions, as is often the case in the annuity market.

Anyone who has visited one of the Disney theme parks knows that there is a massive difference in the excitement level of the various rides and attractions. It’s a Small World? Snooze fest. The Mad Tea Party at Disneyland in California? A recipe for disaster for anyone who may have a weak stomach. For some, the goal is finding the rides that are somewhere in between. If we apply that same thought process to annuity buyers, finding that middle ground can be a challenge.

The It’s a Small World equivalent, a Multi-Year Guarantee Annuity (MYGA), is great. It’s predictable, low risk, and as a result may leave some clients seeking greater potential returns. Given that annuity buyers tend to be risk averse, they often look to another product segment with principal protection and greater upside potential: The Fixed Indexed Annuity (FIA). The problem is that the volatility of returns in an FIA has the potential to be as stomach churning as the Tea Party.

Clients need a middle ground. Something that offers the same principal protection but avoids the possible zero return that can and will occur in a typical FIA. A solution that takes cap rate renewal risk off the table as well. The good news is that this solution does, in fact, exist.

How to Minimize Volatility in an FIA

The first step in minimizing volatility is obvious: The 0% floor offered by FIAs is a great start. That said, it does not eliminate the possibility of a year with no return. For some clients, particularly those whose risk tolerance is somewhere in the middle, a trade of some upside potential for a positive return each and every year is one they would willingly make. They want a less exciting ride than other clients.

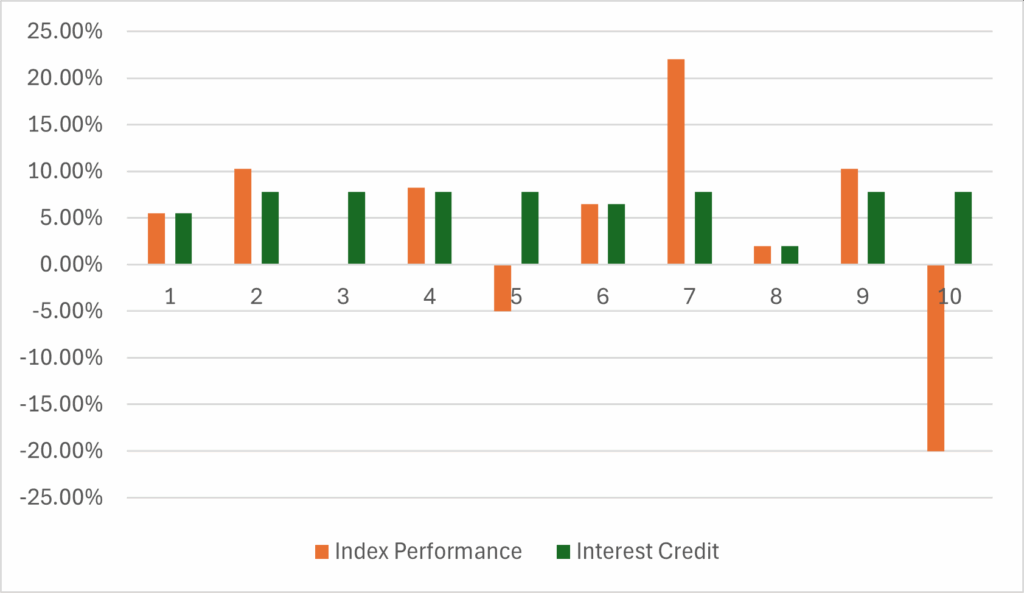

The next question is how to make that a reality? In this case, a slightly lower cap, guaranteed for the entire duration of the contract, allows for a “trigger” in any year with a zero or negative return. What happens when the trigger is activated? The client receives a return equal to the cap rate. That means they receive a return somewhere north of zero, up to the cap, in every contract year. It might look something like Figure 1.

Figure 1: Trigger Mechanics

Figure 1 demonstrates how the returns are less volatile, but what about the overall performance? With volatility somewhere between the typical MYGA and FIA, actual returns will likely land in the same place: Somewhere between the typical MYGA and FIA available in today’s market.

With all of the terms being guaranteed for the life of the contract, this also eliminates one of the challenges of the traditional FIA: Cap renewal rates. In this case, cap rates can be locked in for 7, 10 or even 20 years. All in, this product’s arrival in the market allows for a more nuanced risk tolerance conversation that can result in a more suitable product recommendation for clients seeking a less exciting ride in their financial planning.

Have questions or want to discuss how this applies to your clients? Reach out to your Cavalier Associates Marketing Consultant for additional information.

Not sure who to contact? Please call the office @ (800) 350-2019 for assistance.

Related Articles

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.