Rethinking Life Insurance as a Strategic Asset, Not Just a Death Benefit

Most clients, and many advisors, think of life insurance solely as something you buy to protect your family, business or legacy. While that is undoubtedly the case, it’s far from a complete understanding. The truth is permanent life insurance is a tool that can support multiple financial goals, both today and in the future. In fact, today’s investment climate shines a light on how and why a fixed insurance strategy should be part of a retirement portfolio.

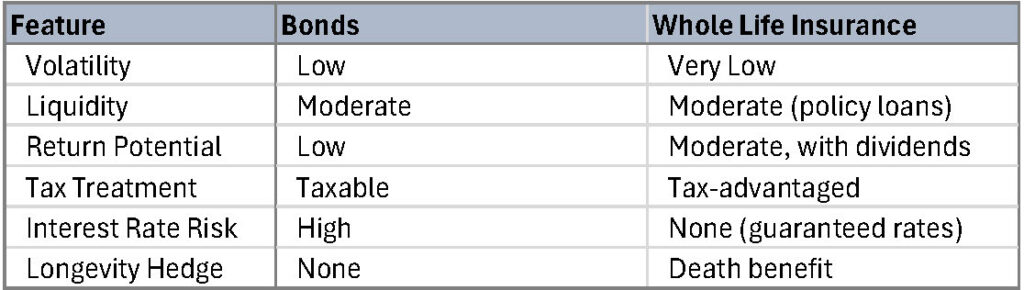

Bonds have traditionally been the go-to option for stability and income in retirement portfolios. That said, today’s incredibly high levels of uncertainty around the economy, tariffs, interest rates and more, make managing a bond portfolio more challenging than ever. Bond investors need to effectively manage credit quality, duration, and liquidity risk in an asset class thought to be safe and predictable. Fortunately, there is an alternative strategy that allows clients to access the same type of investment profile they are seeking from bonds, without the risk and corresponding volatility today’s conditions create. How? By using Whole Life insurance as an alternative to part of their bond allocation.

If the typical allocation for a 45-year-old’s portfolio is in the neighborhood of 70% equities and 30% bonds, integrating Whole Life can be as simple as shifting a portion of the bond allocation to Whole Life. This new portfolio would consist of 70% stocks, 15% bonds, and 15% Whole Life.1,2,3 This combination could reduce volatility, improve long-term outcomes, and offer flexibility that traditional bonds can’t match. A Whole Life policy offers:

- Principal Protection

- Stable, non-corelated returns3

- Immediate liquidity with no volatility

- Total control of if and when taxes are paid

- Creditor protection in some states

- Death Benefit as a built-in hedge

How does this compare to a bond position? See Table 1, Whole Life vs. Bonds for a side-by-side comparison.

Table 1: Whole Life vs. Bonds

Even better, in years when the market is down, policy cash value can supplement retirement income—without selling other investments at a loss. And if the client doesn’t need to use their cash value for income, the death benefit will create a tax-free legacy for their family. All of this from an asset backed by some of the strongest financial institutions in the world: Mutual Insurance Companies.

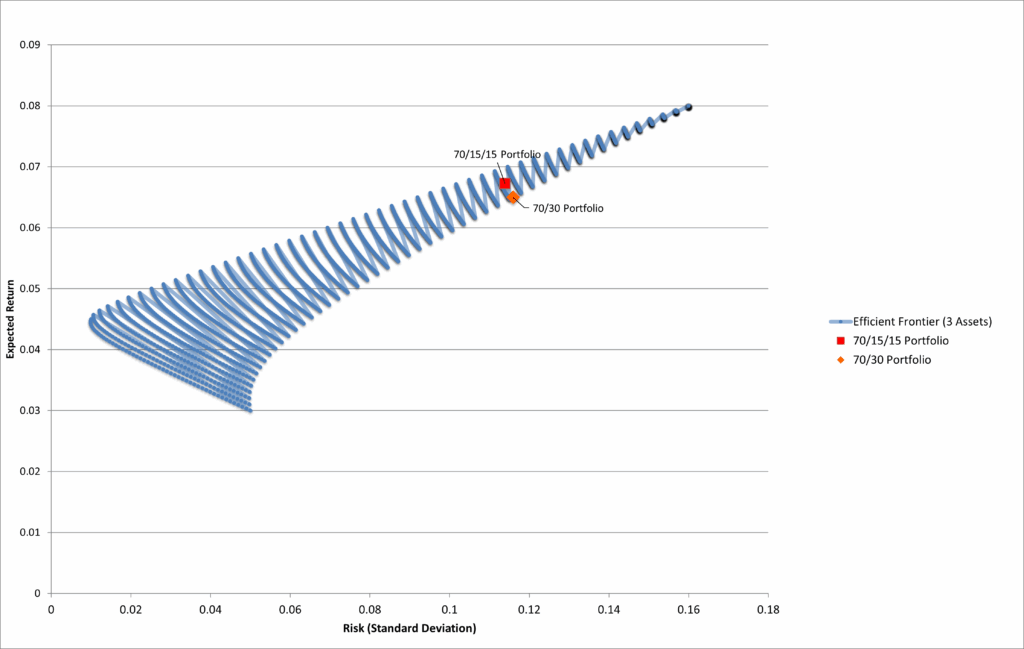

Of course, all of those other benefits become less important if the performance isn’t there. Over the long haul, the performance of a Whole Life policy from a top insurance company approximates that of a laddered bond portfolio. How does this 70%/15%/15% allocation stack up against the traditional 70%/30% approach? A quick look at the Efficient Frontier shows the integration of Whole Life offering slightly better returns for the same or even lower levels of risk.

Figure 1: Efficient Frontier: Stocks, Bonds & Whole Life

Even with all of those benefits, Whole Life isn’t a fit for everyone. It requires commitment, consistent funding, and good health. But for clients with a long time horizon, moderate risk tolerance, and a desire for stability it can be a powerful part of a retirement plan. One that the client’s future self will be incredibly happy to own.

Footnotes

1 Equities are assumed to have a 6.5% average annual return with approximately 15% volatility, based on long-term historical performance of diversified U.S. stock indexes (e.g., S&P 500), adjusted for moderate expectations.

2 Bonds are assumed to have a 3.0% average annual return with about 5% volatility, reflecting intermediate-term investment-grade bond yields.

3 Whole Life Insurance is assumed to produce a 4.5% internal rate of return (IRR) by age 65, net of costs, based on a participating policy from a leading mutual insurer. The return reflects long-term holding with consistent premium payments and assumes favorable dividend performance.

Have questions or want to discuss how this applies to your clients? Reach out to your Cavalier Associates Marketing Consultant for additional information.

Not sure who to contact? Please call the office @ (800) 350-2019 for assistance.

Related Articles

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.