Succession Solutions for Single Owner Businesses

The lack of a second business owner does not eliminate the need for effective buy/sell planning. A well thought out, formal agreement with proper funding can still accomplish the owner’s goals for the business upon their retirement, disability or death.

In discussions about the business market, there is frequently a comment that reflects an advisor mindset that may not be completely accurate: “I’m not in the business market.”

In most instances, even though the advisor making that statement may not be a group benefits or qualified retirement plan expert, nearly 100% of these advisors have business owners as clients. That leads to another nearly universal truth: For these business owners, business and personal planning are intertwined. That fact makes maximizing the value of their business as part of their retirement and estate planning an important objective, and one that demands effective guidance from their advisor.

A place where that can break down is the buy/sell agreement. We’ve all heard the stories of businesses without a plan in place, and one of the frequent causes is the lack of a clear successor. That, like so many other things in our business, can be overcome with the right planning. The most effective approaches address both the planned and the unexpected triggering events and can employ the leverage of life insurance to create or augment a funding strategy.

Consider the business owner whose business is their primary asset and is without a clear successor.

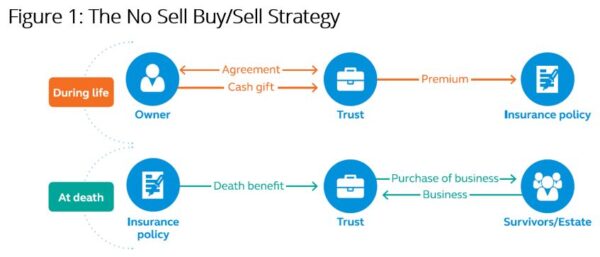

Most advisors would likely think about finding an outside buyer. If all goes to plan, that can absolutely work, but the unplanned exit remains a challenge. The “No Sell Buy/Sell” strategy can be part of a solution to this challenge and uses many of the traditional elements of a buy/sell agreement, with one significant exception: The business owner controls both sides of the transaction. More specifically, a trust they establish, and control becomes the buyer of the business, funded by life insurance proceeds.

This No Sell Buy/Sell involves some of the fundamentals seen in a traditional buy/sell agreement between two owners:

- Establishing a fair value for the business

- Funding the plan with a life insurance policy

It also serves as a way to buy the surviving family members time. The family can still control the business through their control of the trust. If, the business is ultimately sold to an outside party, it will be at a time and at terms of their choosing. The infusion of cash from the initial sale of the business to the trust provides the liquidity they need to be patient if that is what is best for the family. Further, if the business is ultimately sold to an outsider for less than the family hoped, those life insurance proceeds serve to make them whole relative to their prior valuation of the business. Depending on the client’s other planning objectives, this strategy can also integrate with their retirement and estate planning. Please see Figure 1, The No Sell Buy/Sell Strategy, for an overview of the approach.

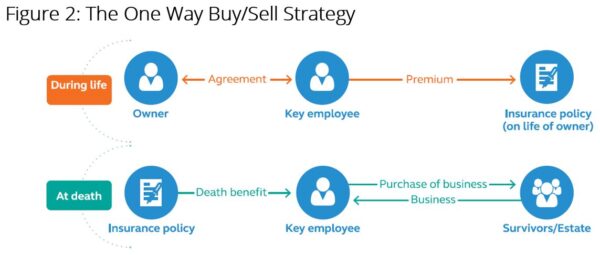

Of course, in some cases, there is a Key Employee who would love to take over the business, but they may not see a way to make it happen. This is where effective planning can again overcome a rather common obstacle.

In this situation, there is an opportunity to take a more traditional approach, complicated only by the fact there is not a second owner of the business also seeking to implement a buy/sell agreement. Instead, the designated Key Employee plays the part of the second owner. The key difference is that the Key Employee does not have an ownership position in the company, making this a “one way” buy/sell agreement. Aside from that difference, the mechanics are much the same as they would be in a traditional buy/sell agreement between two owners.

The Key Employee purchases a life insurance policy on the owner of the business. They Key Employee is the policy owner, is responsible for the premium payments and is also the policy beneficiary. At the death of the owner, the life insurance proceeds are used to purchase the business from the owner’s estate per the terms of the buy/sell agreement. If appropriate, the policy can also play a role in a living buyout and may even be funded by the business via deducible bonus payments to the Key Employee. Please see Figure 2, The One Way Buy/Sell Strategy, for an overview of the mechanics.

The approach above, admittedly, relies heavily on life insurance as the primary finding vehicle. The business owner may benefit from an approach that also more directly addresses a living buyout as we see in the Sole Owner Transition Plan. This strategy includes the sale of a small portion of the business at plan inception, and utilizes installments notes and life insurance to protect both the owner and acquiring Key Employee.

Once the Key Employee completes the initial purchase of a small portion of the business, a traditional buy/sell agreement is put in place that serves all the same functions as it would in a multi-owner business. One of the most important elements is the use of life insurance to protect the original business owner in the event the Key Employee passes away or decides to leave the business. The balance of the sale occurs at the typical triggering events, and can be funded via life insurance, installment notes, or a combination of the two. See Figure 3, The Sole-Owner Transition Plan, for additional details.

![]()

Regardless of which of the three approaches outlined here is ultimately implemented, the underlying message remains the same: The lack of a second business owner does not eliminate the need for effective buy/sell planning. Further, the owner may have more flexibility in these cases simply based on their control of the decision-making process. Whether they ultimately involve a Key Employee as the buyer or a trust via the No Sell Buy/Sell, the outcome is the same: A well thought out, formal agreement with proper funding that accomplishes their goals for the business upon their retirement, disability or death.

Complete the form below to request a session with our team.

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.