Can You Spend the Same Dollar Twice?

The Hidden Pitfalls of Indexed Universal Life: Can You Really Have It All?

The answer, of course, is no. Yet, many clients may mistakenly believe otherwise when presented with Indexed Universal Life (IUL) illustrations designed with a “Swiss Army Knife” approach. These illustrations typically show the maximum possible income level, assuming participating loans. While this is not inherently problematic, it becomes a concern when living benefit features play a significant role in the sales strategy.

Understanding the Client’s Perspective

Most clients are drawn to the appeal of a single financial product that offers death benefit protection, supplemental retirement income, and a safety net for long-term care. However, unless advisors take the time to clarify policy mechanics, clients may assume these benefits are independent rather than sourced from the same pool of funds. This misunderstanding often leads to an expectation that living benefits, such as a Chronic Illness or Long-Term Care Accelerated Benefit Rider (ABR), are additional to any income withdrawn from the policy. The reality, however, is quite different: utilizing policy loans for income can significantly limit access to these living benefits.

The Loan Repayment Factor

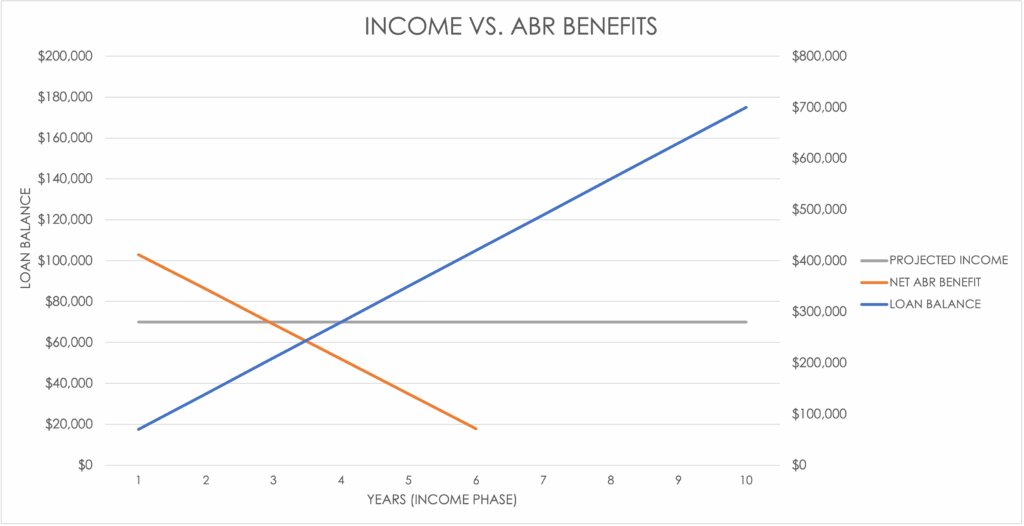

A key factor contributing to this issue is the structure of most ABRs, which typically require partial repayment of any outstanding loans with each benefit payment. Even a modest loan balance can lead to a net benefit that is lower than the income the client was already receiving. Additionally, many ABRs prohibit taking loans and ABR benefits in the same year. Figure 1 below illustrates how quickly an outstanding loan balance can erode the net benefit from the ABR, often reducing it below the policyholder’s expected income within just a few years.

Figure 1: Impact of Loan Balances on ABR Net Benefits

Strategic Solutions

Advisors can help clients navigate these complexities by adjusting the way income is illustrated and withdrawn from the policy. Implementing the following best practices can enhance policy sustainability and benefit accessibility:

- Illustrate Income via Withdrawals First – Rather than relying on loans from the outset, structure income withdrawals to come from the policy’s basis first. This delays the accumulation of loan balances that would later need repayment.

- Delay Income Start Date – Pushing income withdrawals to a later age helps preserve meaningful ABR benefits and minimizes loan balance growth.

- Optimize Claim Timing – Rather than immediately filing an ABR claim when care is needed, consider increasing loan-based withdrawals for a projected five-year period. This often results in a larger net benefit compared to immediate ABR activation, while also reducing administrative burdens and delays associated with claims processing.

The Case for a Multi-Policy Approach

While these strategies mitigate risk, they do not eliminate the fundamental issue that all benefits originate from the same policy pool. For clients who genuinely seek comprehensive protection—death benefits, retirement income, and long-term care—a multi-policy solution is often superior. However, this approach requires a higher financial commitment, which may not be feasible for all clients. In such cases, a well-structured and properly managed single-policy strategy remains a viable alternative.

By proactively educating clients on these nuances and employing thoughtful case design, individuals can maximize their IUL policies while avoiding unexpected limitations on benefits.

Want to Learn More? Complete the form below to request a session with our team.

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.