When a client is declined for life insurance, the conversation doesn’t have to end—it just needs a new direction. An annuity with an Enhanced Death Benefit rider allows you to replicate many of the emotional and financial outcomes of a life policy: a predictable legacy value, guaranteed growth, and a probate-free transfer to heirs—all without medical underwriting.

When a 70-year-old retired business owner applied for life insurance policy with an annual premium commitment of $25,000, he hoped for a straightforward approval. He was financially sound, with plenty of assets in the bank, but his extensive cardiac and other medical history led to a quick and disappointing decline.

The rejection hit hard. He wasn’t looking for income or investment growth—he simply wanted to leave something certain to his two adult children. With his health standing in the way, he assumed the door to guaranteed legacy planning had closed.

That’s when his advisor reframed the conversation. Instead of focusing on what he couldn’t get—traditional life insurance—they explored what he still could: an annuity with an Enhanced Death Benefit (EDB) rider.

Unlike life insurance, this option required no medical exam or health underwriting. It was based purely on financial suitability. The EDB offered a simple promise—guaranteed growth of the legacy value at 10% simple interest each year for up to 15 years, reduced only by withdrawals. At death, his beneficiaries would receive the greater of the EDB value or the contract value, paid directly without probate.

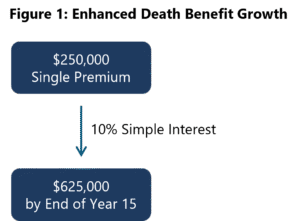

The advisor compared this structure to the original life insurance goal. With a single $250,000 premium, the EDB would grow to $625,000 after 15 years—a number that far exceeded the expected death benefit of approximately $375,000 based on the hoped for Table 4 rating, and one that carried a similar emotional impact

The client liked that his money would stay in his name and under his control. Unlike a life policy, his cash value would continue to grow and be available to him should he need it during his lifetime—though he understood withdrawals would reduce the amount left for his beneficiaries.

To the client, that trade-off felt fair—especially since he was starting from a “declined” position.

Taxation was addressed directly. The advisor explained that while life insurance pays a tax-free death benefit under IRC §101(a), annuity proceeds are treated differently under IRC §72. For a non-qualified annuity, the portion representing the client’s original investment (the premium) is returned tax-free, while any earnings are taxed as ordinary income to the beneficiary when received.

The application process was fast and uneventful. No doctor’s notes, no labs, no waiting for an underwriter’s decision—just suitability paperwork and funding. Within two weeks, his contract was issued.

All in, fifteen years of predictable 10% growth on a protected base gave the client exactly what he wanted: certainty, not speculation. Surprisingly, if he lives to age 75, the annuity solution actually outperforms life insurance at a table 4 rating on a pre-tax basis. If the insured lives another eleven to twelve years, the EDB would grow to the point it would our-perform the life insurance on an after-tax basis as well.

Figure 1: Enhanced Death Benefit Growth

For the advisor, this case became a reminder that legacy conversations don’t end with a life insurance decline. Sometimes, they just need a different chassis. A fixed index annuity with an Enhanced Death Benefit can replicate much of the emotional value of life insurance—guaranteed growth, control, and direct transfer—without the medical barriers that stop so many clients from leaving the legacy they envision.

Have questions or want to discuss how this applies to your clients? Reach out to your Cavalier Associates Marketing Consultant for additional information.

Not sure who to contact? Please call the office @ (800) 350-2019 for assistance.

Related Articles

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.