Can You Insure Against Market Losses?

With the recent increase in frequency and severity of natural disasters, risk management is top of mind for many. Of course, the risks clients face includes other topics, including threats to their portfolios, suggesting an obvious question: Can clients insure their portfolios the same way they do their houses?

Can clients insure their portfolios? Yes. Is that “insurance” truly analogous to their homeowner’s insurance? Obviously not. However, the principle remains the same: Clients can shift risk to other entities as a way of insulating themselves from loss. In some ways, asset managers already do this. Their use of asset classes with different risk profiles dampens the impact of volatility in other positions, increasing the probability of a successful outcome for their clients. In many cases, however, they are leaving one of the most effective asset classes at their disposal out of their strategy.

Permanent life insurance stands out as a particularly effective tool to hedge against excess volatility in other positions. While it’s easy to point to Indexed UL or Variable UL with Indexed or RILA strategies as a potential solution because of the downside protection they offer, they are far from the only solution. In fact, Whole Life is likely the superior choice for clients seeking to mitigate market risk because of the non-correlated nature of the bond-like return Whole Life can deliver. In addition, the tax favored treatment of Life Insurance makes the approach all the more attractive and effective.

The remaining question is simply one of how to implement a risk management strategy using life insurance? Ultimately, it will come down to the individual client, their appetite for risk and the other elements of their asset management strategy. That said, two fundamental approaches are worth consideration.

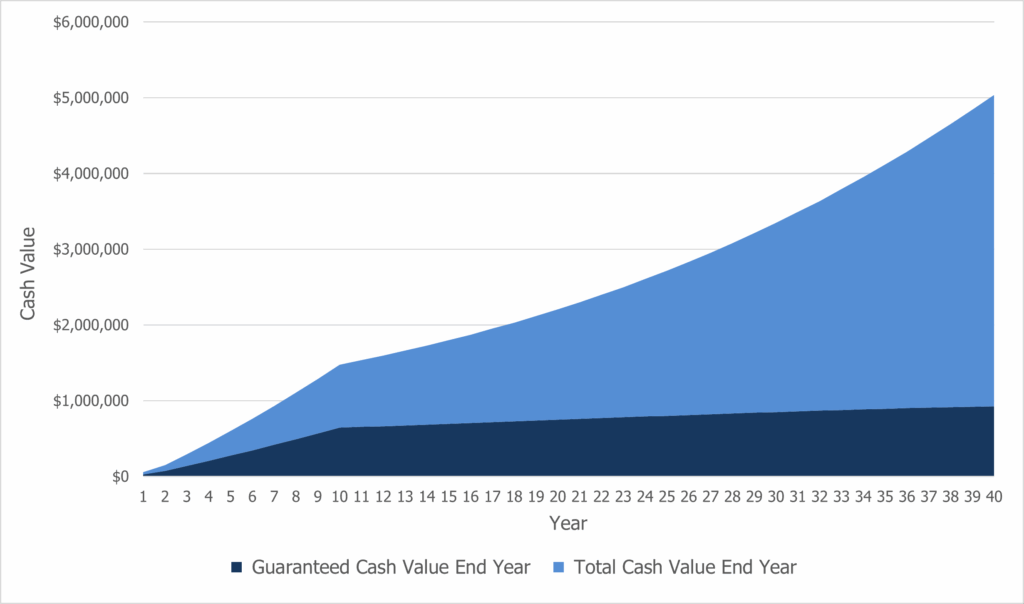

Life Insurance as a Hedge Against Volatility in Other Investment Positions

The first approach is akin to traditional asset allocation and may simply be an extension of an existing bond strategy to provide diversification and a smoother return profile. Why implement this if there is already a bond strategy in place? While Whole Life offers a bond-like return, that return is not driven by the day-to-day performance of the bond market. Think about this as a way to access the type of return a mutual insurance company offering Participating Whole Life sees in their general account, plus any return generated by their other businesses, all reflected in the guaranteed return as well as total return including the dividend. Assuming today’s dividend rates, that return could look something like that seen in Figure 1, below.

Figure 1: Whole Life Cash Value Growth

Cash Values based on a 50-year-old male, preferred health, funding a $1MM Whole Life policy with paid-up additions dividend option. Please contact the office for additional details.

What does Figure 1 translate to in terms of total performance? Consider the following:

- Internal Rate of Return:

-

- Year 10: 1.00%

-

- Year 20: 4.02%

-

- Year 30: 4.60%

-

- Year 40: 4.74%

- Tax Equivalent IRR, assuming a 24% tax rate:

-

- Year 10: 1.32%

-

- Year 20: 5.29%

-

- Year 30: 6.05%

-

- Year 40: 6.24%

There will clearly be an ebb and flow to actual performance over time but based on dividend history and how slowly dividends tend to move over time, this is likely to be far less volatile than a bond portfolio. Additionally, the top tier financial ratings of many mutual insurance companies allow their whole life products to offer the same, if not superior, quality versus many bond offerings. Of course, a bond portfolio fails to offer any type of death benefit. In this case, the total death benefit at age 90 is projected at a robust $4.44MM that passes to the beneficiary tax-free, a 6.54% tax-equivalent IRR.

An Insurance Portfolio Approach

There’s a second approach that can come into play when a client has an outsized need for insurance coverage, likely for their estate or wealth transfer planning. Rather than simply considering a single type of insurance, it makes sense to apply the same thought process around asset allocation in investment management to their insurance strategy. By constructing a portfolio of insurance solutions, each with a unique risk/reward profile, clients will see similar benefits in terms of lower volatility and overall performance. Whole Life plays the same role in this approach, offering the bond-like return without the volatility that comes with direct investment in the bond markets.

In addition, as actual performance plays out over time, advisors and their clients can make better decisions around how to allocate policy cash values, changes to premium flows and the like. Decisions based on actual performance and the inevitable positive or negative variance from the initial sales illustration. The result is an insurance portfolio that can be actively managed to increase the probability of a successful end result for clients.

Regardless of which of these two approaches, or others, are used, the message is the same: Clients face real risks in their asset management strategy, and permanent life insurance, particularly Whole Life, can be used to insure against those risks. As with any type of insurance, it needs to be implemented before the loss occurs, making now the perfect tie to implement a life insurance position in a client’s financial plan, before the next market correction is upon us.

Have questions or want to discuss how this applies to your clients? Reach out to your Cavalier Associates Marketing Consultant for additional information.

Not sure who to contact? Please call the office @ (800) 350-2019 for assistance.

The contents of this document should not be considered as tax or legal advice. Any information or guidance provided is solely for educational or informational purposes and should not be relied upon as a substitute for professional advice. It is always recommended to consult with a licensed financial or legal advisor for specific guidance related to your individual situation.